ESG reporting

Measuring environmental, social and governance (ESG) factors

Environmental, social and governance (ESG) factors can be used as a framework for reporting on a firm’s sustainability performance. Similar to Corporate social responsibility (CSR) or corporate sustainability reporting, ESG reporting can help a company communicate its contribution to sustainability through KPIs to reach environmental, social and governance objectives within the firm.

Reporting on ESG factors is also important for external communication to customers and investors. Many investment banks have now set their own ESG guidelines to mandate the compliance and screen their investments, and to distinguish those with the best sustainability performance. Performing well in terms of ESG principles, can therefore attract or maintain outside investment.

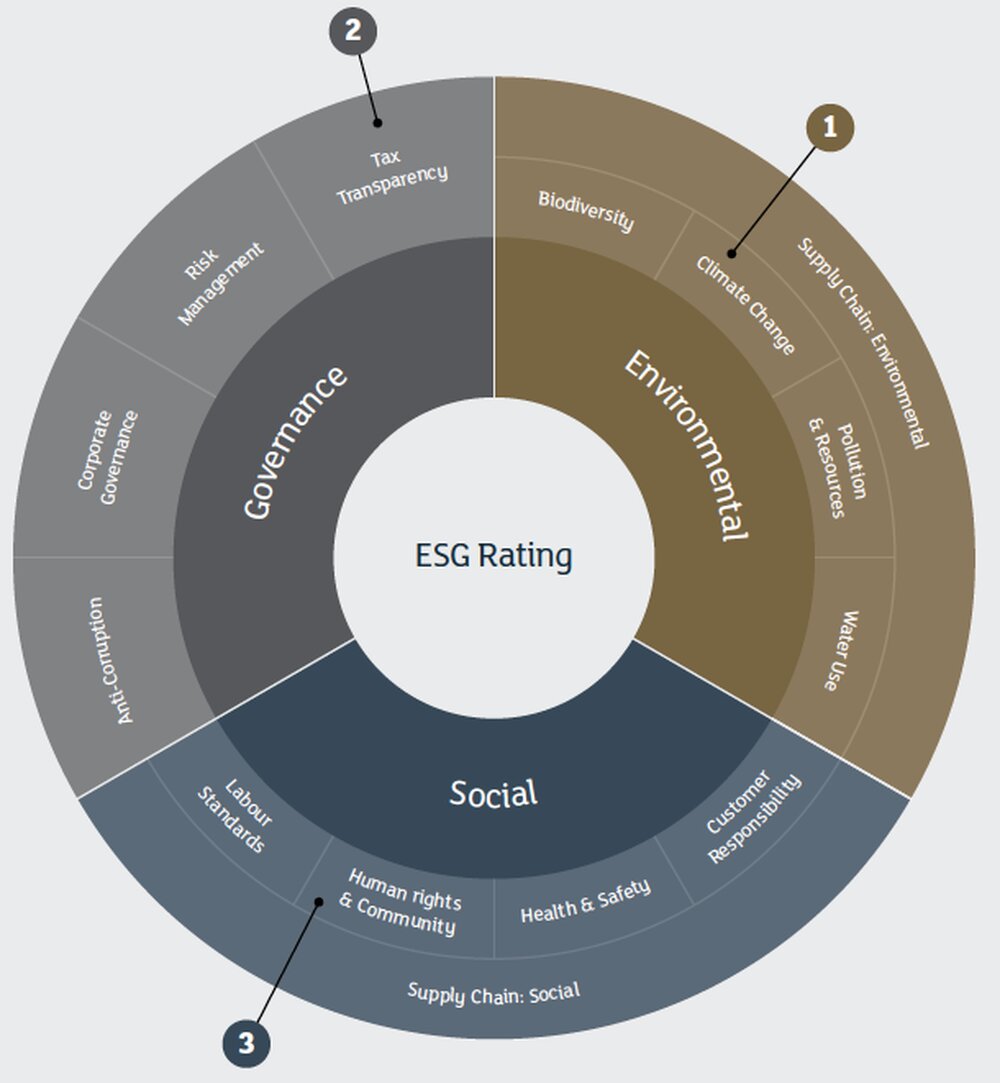

Examples of Environmental criteria include:

- Natural resource conservation

- Energy and resource use

- Waste management

- Pollution and emissions

- Biodiversity preservation

Social criteria are related to the company’s relationships with employees, customers and stakeholders. Factors can include:

- Supplier selection – Do their suppliers meet their sustainability objectives?

- Health & safety of employees

- Working conditions

- Relationship to the local community and other stakeholders

Governance factors relate to the internal processes of reporting and accounting, and surround ideas of:

- Transparency

- Accuracy

- Communication with stakeholders

- No illegal activities or corruption

ESG model over Environmental, Social and Government factors. Source: www.ftserussell.com/esg

ESG model over Environmental, Social and Government factors. Source: www.ftserussell.com/esg

The following examples explain the investment case related to climate change (E), Human rights & community (S) and Tax transparency (G). They are taken directly from the London Stock Exchange’s 2018 Guide to ESG Reporting for demonstration purposes.

1. CLIMATE CHANGE

The investment case

Investors often want to understand whether businesses can:

- successfully respond to climate change risks;

- demonstrate future viability and resilience; and

- achieve cost savings through efficiencies and identify opportunities through green revenue opportunities.

The sources of investment risks

Key sources of investment risk and opportunity:

- regulatory: standards, taxes, carbon pricing;

- market: reduced demand for high-carbon goods, products and services

- and decreased capital availability for high carbon products;

- market: increased demand for low-carbon goods, products and services;

- capital: increased capital availability for low-carbon services

- and technologies; and

- weather: natural disasters and resource risks.

Example indicators of practice and performance

- Three years of total energy consumption data

- Board oversight of climate change: a) Evidence of board or board committee oversight of the management of climate change risks, b) Named position responsible at Board Level

2. TAX TRANSPARENCY

The investment case

Investors often want to understand whether businesses can:

- not only comply with tax arrangements, but also have a strong governance process and transparency around their tax policy and tax arrangements; and

- demonstrate commitment to transparency by engaging with stakeholders and the public to communicate their contribution to local economies.

The sources of investment risks

Key sources of investment risk and opportunity:

- regulatory: risks of increased regulation which could close particular tax arrangements, referred to by some as ‘loopholes’ which would mean reduced margins and profitability of particular companies. In some cases it may even affect a company’s ability to operate in certain markets; and

- reputational: increased scrutiny of corporate tax behaviour.

Example indicators of practice and performance

- A policy OR commitment to: a) Tax transparency or tax responsibility, b) Align tax payments with revenue-generating activity, or reduce or refrain from the use of offshore secrecy jurisdictions for the purposes of tax planning

- Board has oversight of tax policy: a) Evidence of board oversight of the management of tax risks, b) Named position responsible at Board level

- Disclosure of corporation tax paid globally: a) With at least domestic and international breakdown, b) With country by country breakdown

3. HUMAN RIGHTS & COMMUNITY

The investment case

Investors want businesses that:

- engage in active discussion around human rights and community issues;

- demonstrate operational robustness and reputational resilience by addressing their impact on the communities in which they operate; and

- Have strong and positive relationships with communities.

The sources of investment risks

Key sources of investment risk and opportunity:

- regulatory: costs associated with regulatory compliance;

- market: increased exposure to human rights risks in supply chain;

- reputation: risks caused by community relations and human rights issues; and

- operations: increased chance of operational shut downs or revocation of licenses, if the local community resists or protests the presence of the business.

Example indicators of practice and performance

- Stakeholder engagement to verify human rights risks and impacts: a) Evidence of consultation taking place, b) Documented meetings OR reports of how results have been used

- Qualitative: Total amount of corporate or group donations/community investments made to registered not-for-profit organisations.